Benefits of Non-Owners Car Insurance: What is it & Who Should Buy a Policy?

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

Heidi Mertlich

Licensed Insurance Agent

Heidi works with top-rated insurance carriers to bring her clients the highest quality protection at the most competitive prices. She founded NoPhysicalTermLife.com, specializing in life insurance that doesn’t require a medical exam. Heidi is a regular contributor to several insurance websites, including FinanceBuzz.com, Insurist.com, and Forbes. As a parent herself, she understands the need ...

Licensed Insurance Agent

UPDATED: Dec 9, 2022

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

UPDATED: Dec 9, 2022

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

Every driver needs an auto insurance policy to keep them protected while behind the wheel.

But do the same rules apply to drivers who do not have a car?

Some individuals who only drive occasionally choose to borrow or rent a car from friends or family members when they need to drive.

But the fact that they do not own an automobile doesn’t take away their responsibility to be a safe driver and handle the consequences if they cause an accident.

That is where a non-owner policy can be helpful.

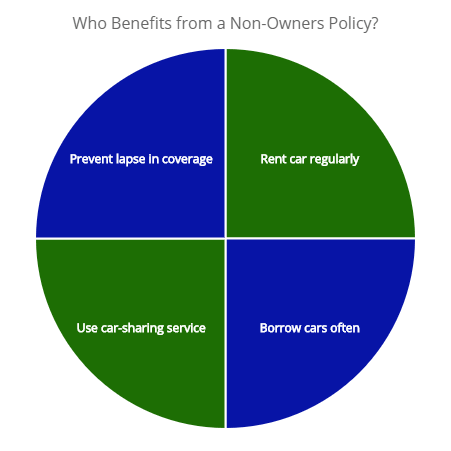

Illustrated above are the most common reasons a non-owner driver would need a non-owner policy as a secondary policy for continuous coverage. And to supplement the primary driver’s minimum liability coverage. Another reason is if a person doesn’t own a car and is required by a court for a DUI or reckless driving.

Illustrated above are the most common reasons a non-owner driver would need a non-owner policy as a secondary policy for continuous coverage. And to supplement the primary driver’s minimum liability coverage. Another reason is if a person doesn’t own a car and is required by a court for a DUI or reckless driving.

Non-Owner Car Insurance: What is it?

A non-owners insurance policy, sometimes called non-drivers insurance, provides continuous coverage to motorists who do not own the vehicle they are driving.

Suppose the driver is behind the wheel of a car that doesn’t belong to them, and they are involved in an accident that causes bodily or physical damage.

In that case, a non-owner auto insurance policy will take care of medical bills or automobile repair costs.

Besides property damage and bodily injury liability, a policy can cover:

- Medical payments coverage

- Personal injury protection

- Uninsured motorist protection

- Underinsured motorist coverage

- Rental car liability protection

There is no specific vehicle assigned to a non-owner car insurance policy; therefore, it will not include comprehensive and collision coverage.

The non-owner policy will not cover damages to the vehicle you are driving.

And it will not cover injuries or medical bills for you in the event you are in an automobile accident or collision.

Below are some of the reasons or benefits you should consider non-owners car insurance to supplement an existing liability policy.

| Reason | Benefit |

|---|---|

| You rent cars regularly | It offers liability coverage on rental vehicles. It can be a way to reduce expenses. |

| You borrow cars often | If you borrow cars often that aren't in your household. You would supplement the existing vehicle's policy. |

| You use a car-sharing services | If you a member of a car-sharing service like Car2Go, Zipcar or Maven. They offer coverage, but you want to supplement their coverage for additional protection. |

| Lapse in coverage | If you don't want to have a lapse in coverage you buy a non-owners policy. If you do have a lapse in protection insurers may consider you high risk and you will have an increase in rates when you purchase a policy. |

| You’re required by a court | A court may require you to file a proof-of-insurance certificate to maintain your driver’s license. This usually happens when you are convicted of a DUI or reckless driving when you don't own a car. Then you would need non-owners SR-22 insurance. Or a FR-44 in Florida or Virginia. |

Non-Owner Car Insurance: What to Know

Based on statistics from the US Office of Highway Policy Information, the number of motorists with a valid license in the country has increased from 163 million people in 1988 to 210 million as of 2010.

And according to details from the US Department of Transportation, 8% of all licensed motorists do not drive a car that they own.

Households with an income lower than $25,000 are more likely not to own an automobile than families that earn more than $25,000 annually.

And drivers who rent their homes are also more likely not to own a car than those who own homes.

These statistics also apply to condo or apartment renters.

When you also consider than around 19% of all single-person households do not own vehicles, it makes sense that non-owner auto insurance policies exist.

| This is how a non-owners policy works. You borrowed your friend's vehicle which has $20,000 in liability protection. You bought a non-drivers policy with $40,000 in liability protection. If you had an accident with your friend's vehicle causing $25,000 in damages you would be responsible for the extra $5,000. Your non-drivers policy will cover the $5,000 in excess damages. The non-drivers policy needs to cover beyond what the vehicle owner's liability coverage is. Otherwise your non-drivers coverage would not cover the excess damages. |

Who Needs a Non-Owners Policy?

Non-owner insurance policies are designed for licensed motorists who do not own a car but still need liability insurance.

Here are a few examples of individuals who would need a non-owners insurance policy.

– Licensed drivers who are not vehicle owners but drive rental cars often.

– Having this coverage plan allows motorists to pay a more affordable rate for the insurance required by their car rental company.

– Anyone who doesn’t own a vehicle and is trying to get their driver’s license in a state that requires you to have proof of insurance.

– A motorist who often borrows a vehicle from their friends, neighbors, coworkers, or anyone who doesn’t have them listed as an insured driver on their policy.

– Anyone who has been insured for a long time but is currently in-between cars.

– The non-owner policy is a great option to help you keep your insurance coverage current while you shop around for a new car.

– A licensed driver under suspension must file a financial responsibility certificate, but they do not own a car.

How a Non-Owner Insurance Policy Can Benefit You

There are several great benefits associated with this type of affordable policy.

Here are just a few of the advantages you can expect from this type of coverage.

Cheaper Insurance Rates

The policies are more affordable than standard coverage because the amount of time the motorists spends on the road is much less.

Depending on the driver profile, the cost of coverage is from $200 to $500 annually, according to WalletHub.com.

Drivers who don’t own cars can take advantage of these lower premiums while still having access to the coverage they need whenever they need it.

Which company is best for you depends on your driving history and personal information.

You want to get at least three insurance quotes from three different auto insurance companies.

Below is the countrywide average cost by insurer:

| Company* | Annual Cost for 25-year old | 45-year old |

|---|---|---|

| USAA | $412 | $252 |

| Liberty Mutual | $465 | $276 |

| State Farm | $477 | $231 |

| Geico | $440 | $230 |

| Nationwide | $439 | $243 |

| Progressive | $455 | $311 |

| Farmers | $487 | $327 |

| Travelers | $512 | $389 |

| Elephant | $487 | $368 |

| Auto-Owners | $535 | $321 |

| Hartford | $487 | $298 |

| Ameriprise | $412 | $289 |

*The cost of coverage is for bodily injury liability and property damage liability as secondary coverage to the vehicle owner’s primary policy. Suppose you want add-ons such as uninsured motorists protection (UM), underinsured motorists coverage (UIM), personal injury protection (PIP), or medical payments coverage (MedPay). In that case, it will possibly cost more, as illustrated. Some companies do not provide policy options or limited availability in some states.

More Convenient

A non-owner auto insurance plan allows those who do not often drive to get the most out of their driving time at a lower cost.

If you live in a big city, owning a car may be out of the question due to the high costs of parking at a garage.

But activities such as driving to visit friends or making a large purchase at a store can be much easier when you have a car to drive.

Suppose you don’t want car ownership responsibility but still want the freedom to drive whenever possible. In that case, a Non-Owners Car Insurance plan is a great insurance option and possibly the cheapest for short-term driving.

Instant Rental Car Insurance

Most traditional auto insurance policies do not cover rental cars.

To ensure you have auto insurance coverage while renting a vehicle, you would need to purchase an additional, temporary policy or rental car insurance.

But, when you have a non-owners insurance policy, there is no need to buy an additional plan.

Your rental car and any accidents that occur while you are driving it are covered.

When you rent a car, be sure to:

– The non-owners policy will have liability protection while you are driving the vehicle. Call your insurer to verify.

– Check with your credit card company if damages cover your rental vehicle. You may have to purchase a collision damage waiver from the rental company to be on the safe side.

Zero Gaps in Coverage

Having gaps in your insurance coverage, regardless of your reason, can cause you problems as a driver and a future car owner.

Some dealerships will look at your auto insurance history and notice when you didn’t have coverage for long periods.

This information could cause you to seem like a high-risk driver, which could lead to higher rates.

When you have a non-owner liability auto policy, you can avoid these issues because insurers will see that you are responsible drivers who have maintained coverage over the years.

Qualifications for Non-Owners Auto Insurance

Generally speaking, non-owner insurance policyholders are drivers who do not have a car, but they do drive on occasion.

Because most states require all motorists to have some form of coverage, they are a good solution.

Here are a few of the factors that most drivers with a non-owner auto insurance plan have in common.

This type of insurance is ideal for drivers who only drive on occasion but still want to avoid gaps in their coverage.

Keep in mind some insurance providers view a lapse in coverage as a sign the driver is high-risk.

Drivers who borrow or rent vehicles to drive may need this form of coverage.

Sometimes a car rental company will offer insurance coverage on the rental car used.

However, this additional coverage can be costly.

Having this type of policy already in force can help you avoid any other fees.

Individuals who need to show proof of insurance to obtain their license or reinstate coverage can benefit from having this type of auto policy.

In some states, it is required that drivers get this coverage before they can obtain their license.

Other states might require a driver to get the coverage when they get an SR-22 or an FR-44.

Where to Buy and What it Covers

To get a quote for non-owner insurance, you will need to either make a call to your preferred insurance provider or visit the agency in person.

Keep in mind some providers will only offer the policies to their existing customers.

And while most major carriers such as Progressive, Farmers, and Nationwide, offer this type of coverage, some, such as Allstate, do not.

FAQs

What is Covered Under Non-Owner Car Insurance?

This insurance provides coverage for bodily injury and property damage liability when driving a vehicle, you do not own.

There is other protection available, such as personal injury protection, but it depends on the state.

What Isn’t Covered by the Policy?

Most non-owner insurance policies do not cover spouses of the driver or other household members, a car owned by you, cars you use for your business, or medical expenses for yourself and your passengers if you are at fault.

What is the Cost of Coverage?

Insurance rates can vary by the amount of liability chosen and if you have a file in the motor vehicle records database.

Those who have moving violations may endure higher rates.

How Can I Get Non-Owner Car Insurance?

Several major insurance providers offer non-owner auto insurance policies. Getting in touch with your local agency to find out what is offered can save you a lot of time.

Do Non-Owner Car Insurance Policies Have a Deductible?

Typically, these policies do not have a deductible.

That means you do not have to pay any money out of pocket before your coverage begins.

That is because the coverage is looked at as secondary coverage only used if the car owner’s insurance policy is not sufficient to cover the damages.

Is Non-Owner Auto Insurance the Same as Rental Insurance?

While the coverage may be similar, non-owner insurance is not the same as renter’s insurance.

With this type of policy, you have coverage for any vehicle you drive and do not own.

With renter’s insurance, you are covered for accidents in the specific vehicle you are renting.

Do I Need the Protection if the Car Owner has a Policy?

Yes, it would help if you still had non-owner insurance because it will kick in after the owner’s insurance policy has been exhausted.

Does it Help with PIP Coverage?

It depends on the policy and insurance company.

Still, some policies pay for medical payments or personal injury protection for injuries either you or your passengers endure during an accident where you were at fault.

To learn more about the many benefits of the coverage, get in touch with our experts today.

Our licensed professionals will be happy to answer any questions you have.

Sources

https://www.fhwa.dot.gov/policyinformation/

https://www.transportation.gov/

{“@context”:”https://schema.org”,”@type”:”FAQPage”,”mainEntity”:[{“@type”:”Question”,”name”:”What is Covered Under Non-Owner Car Insurance?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”This insurance provides coverage for bodily injury and property damage liability when driving a vehicle, you do not own. There is other protection available, such as personal injury protection, but it depends on the state….learn more about Non-Owners Car Insurance.”}},{“@type”:”Question”,”name”:”What Isn’t Covered by the Policy?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”Most non-owner insurance policies do not cover spouses of the driver or other household members, a car owned by you, cars you use for your business, or medical expenses for yourself and your passengers if you are at fault….More“}},{“@type”:”Question”,”name”:”Do Non-Owner Car Insurance Policies Have a Deductible?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”Typically, these policies do not have a deductible. That means you do not have to pay any money out of pocket before your coverage begins. That is because the coverage is looked at as secondary coverage only used if the car owner’s insurance policy is not sufficient to cover the damages….Learn more about Non-Owners Car Insurance.”}},{“@type”:”Question”,”name”:”Is Non-Owner Auto Insurance the Same as Rental Insurance?”,”acceptedAnswer”:{“@type”:”Answer”,”text”:”While the coverage may be similar, non-owner insurance is not the same as renter’s insurance. With this type of policy, you have coverage for any vehicle that you drive and do not own. With renter’s insurance, you are only covered for accidents in the specific vehicle you are renting…More“}}]}

Free Auto Insurance Comparison

Enter your ZIP code below to view companies that have cheap auto insurance rates.

Heidi Mertlich

Licensed Insurance Agent

Heidi works with top-rated insurance carriers to bring her clients the highest quality protection at the most competitive prices. She founded NoPhysicalTermLife.com, specializing in life insurance that doesn’t require a medical exam. Heidi is a regular contributor to several insurance websites, including FinanceBuzz.com, Insurist.com, and Forbes. As a parent herself, she understands the need ...

Licensed Insurance Agent

UPDATED: Dec 9, 2022

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident auto insurance decisions. Comparison shopping should be easy. We are not affiliated with any one auto insurance provider and cannot guarantee quotes from any single provider. Our partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.